Porsche AG (P911): The Selloff Is Overdone - But I Am Not Buying Yet

From 80% EV by 2030 to a full strategic reversal in three years. Porsche paid a steep price for a bet that did not work. Now the question is whether the worst is behind them.

The whole German car industry has been going through rough waters for some time now. The reasons are many, but I think it is the right moment to reassess what is happening across the industry and prepare positions for when the inflection point finally arrives. I started this series with a company I already hold a position in Mercedes-Benz Group (MBG) and have now turned my attention to a new one: Porsche AG (P911).

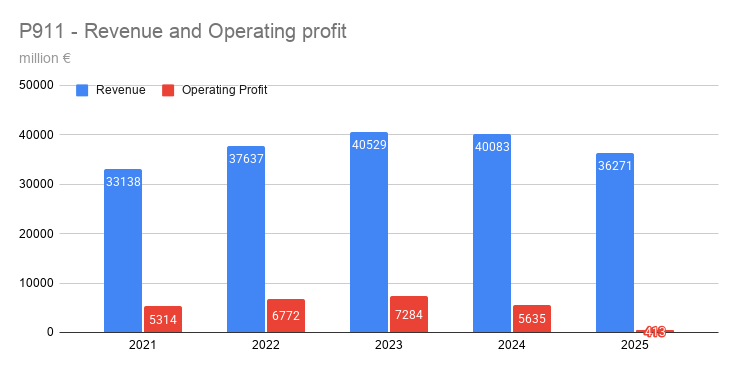

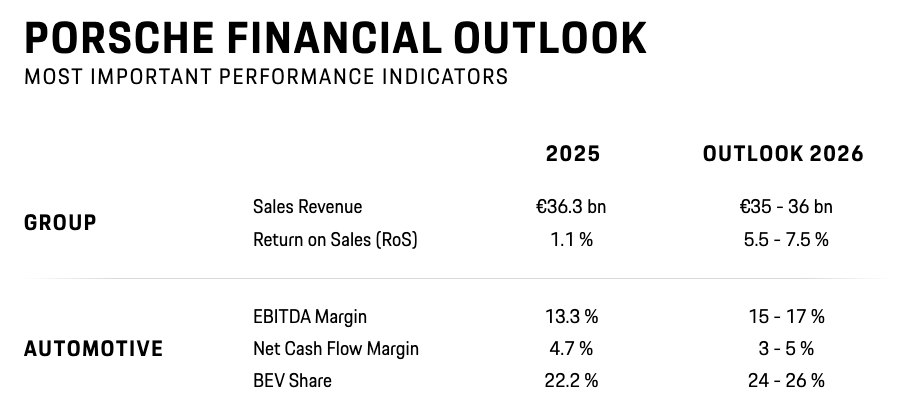

As one of the most famous luxury and performance carmakers in the world, Porsche holds an interesting position with a strong economic moat. Annual revenue currently stands at around €36.3 billion, which is just under 10% below last year's figure. At the same time, operating margin dropped to 1.1% — a steep fall from the 14.1% reported in 2024.

While the drop in operating profit looks alarming on the surface, it is worth noting that a large part of it would not have occurred without extraordinary expenses falling into three categories: the realignment and rescaling of the company, additional costs related to battery activities, and US tariffs. Together these total €3.9 billion. Strip them out and operating profit would have been around €4.3 billion, implying a margin closer to 12%; far more in line with previous results. For context,

Ferrari's operating margin sits between 25% and 30% over the same period, which tells where the ceiling is if Porsche ever achieves Ferrari-like brand discipline.

One structural point worth flagging before going further: P911 shares carry no voting rights. VW controls 75.4% of the ordinary shares, meaning capital allocation decisions ultimately rest with them — not with minority investors. This is not a deal-breaker, but it is something that should be reflected in how you price the stock.

The China Collapse That No Recovery Plan Can Easily Fix

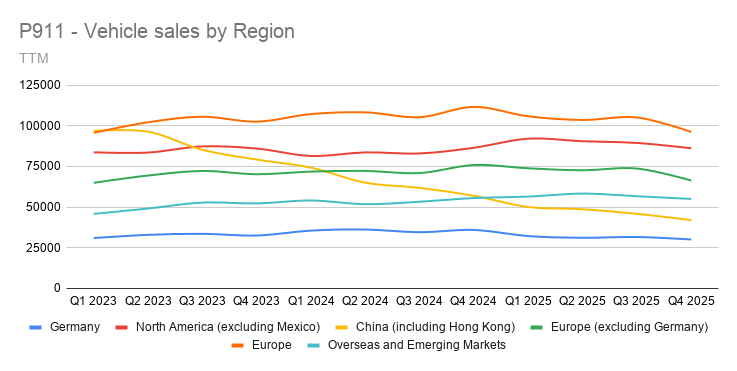

Vehicle sales are declining across all regions, but the sharpest drop is in China. A 26% fall in a single year is not "just a cyclical dip", it is a structural problem. Chinese domestic brands are now seriously disrupting the luxury and premium segment, and they are doing it at significantly lower prices.

I do not think we will see China sales return to previous levels anytime soon. For Porsche to reclaim that ground, it would need to fundamentally rethink both its pricing model and the perceived quality of its products relative to local competition. For a European company, that is practically impossible to do quickly. The decision to cut the dealer network from 150 to 80 locations and wind down the proprietary charging network are clear signals that management is no longer treating China as a growth market. They are managing a controlled retreat.

Other regions are either stagnating or growing too slowly to compensate for the China decline. Germany is mostly flat and slowing. North America faces a significant headwind from US import tariffs. During last year, Porsche absorbed roughly €700 million of that cost itself, treating it as a one-off. If tariffs remain or escalate, that burden becomes a recurring expense rather than an exceptional one.

Porsche's EV Strategy: A Bold Ambition That the Market Rejected

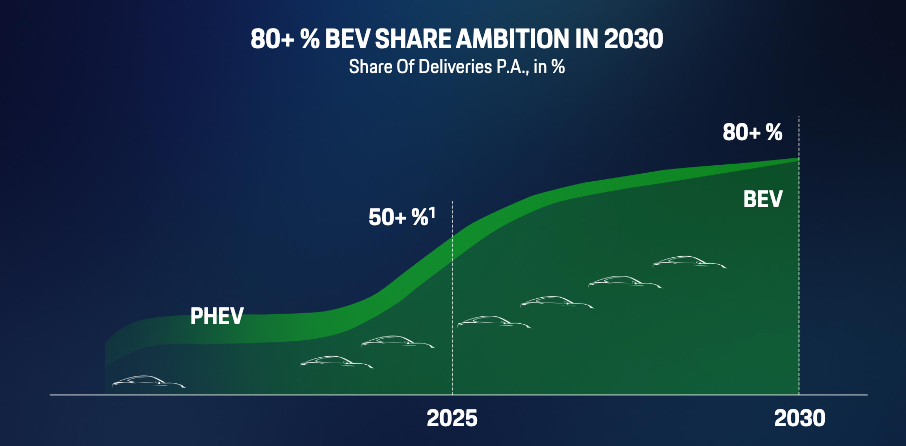

One of my biggest concerns going into this analysis was Porsche's EV strategy or, more precisely, what it cost them to abandon it. Back in 2022, the company announced that 80% of its vehicles would be fully electric by 2030. At the time, with the Taycan's strong launch fresh in memory, this was a bold but not unreasonable goal — it is worth remembering that the Taycan actually outsold the iconic 911 in 2021.

Only a few years later, reality hit hard. CEO Oliver Blume walked back the 80% EV target, and the "reversal" came with a bill to pay. Many models had been designed from the ground up as pure EVs, built on platforms with no space for a combustion drivetrain. Converting and adapting them back is expensive and time consuming. This is one of the primary reasons the 2025 results carry such large one-off charges. New CEO Michael Leiters has now confirmed that combustion and hybrid options will return across the lineup.

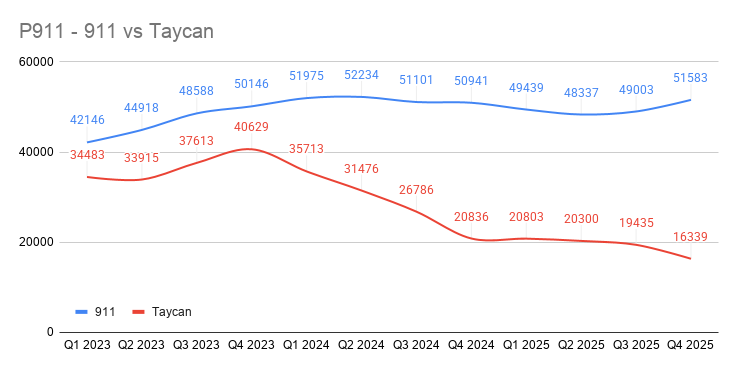

To understand the scale of the EV misstep, it helps to look at what happened to Taycan and 911 sales side by side throughout this period. The 911 was always combustion-powered, and it was precisely the model that the Taycan was supposed to eventually replace. Instead, the opposite happened. Taycan peaked at over 41,000 units in 2021 and has since collapsed to around 16,000 by 2025, a decline of nearly 60% from its best year. The 911, meanwhile, kept growing and reached around 52,000 units in 2025. The market delivered a very clear sign, and Porsche is only now fully accepting it.

Stabilisation, Not Recovery. Here Is What Could Still Go Wrong

The guidance for 2026 is not a recovery story. To say it optimistically, it is a stabilisation story. Revenue is projected at €35 to €36 billion, which is flat to slightly down from 2025. A meaningful rebound this year looks unlikely, particularly given the geopolitical uncertainty that has intensified over the last two months.

One-off charges will continue into 2026, most likely in the range of €200 to €500 million. That is not a small number on top of an already compressed margin. The China problem remains unsolved, and I am not fully convinced that management has a clear answer for how to address it structurally, cutting the dealer network is a defensive measure, not a growth strategy.

As an example of organisation issue on a product level, the 718 gap is a real problem. ICE production ended in October 2025, the electric replacement is not arriving until late 2027 at the earliest, and hybrid or combustion variants of the new generation are not expected before 2028 or 2029. That is a two to three year window where one of Porsche's entry-level sports cars simply does not exist as a new product.

The dividend cut is also worth acknowledging. Porsche was historically attractive partly because of its yield. The reduction from €2.31 to €1.01 per preferred share brings the yield down to around 2.5% at current prices. Meaningful, but no longer the shining star in portfolio.

A Company Worth Watching, Not Yet Worth Buying

It is still too early to build a meaningful position in P911. The headwinds are real and the visibility on recovery is limited. That said, the new CEO brings genuine credibility. Leiters built his name at Ferrari and McLaren, not in a boardroom, and his instinct to move Porsche upmarket rather than simply manage a decline is the right one.

The shift away from an EV-only performance strategy and the serious speculation around a hypercar above the 911 are both encouraging signals. If Leiters can position Porsche closer to Ferrari's model. Fewer units, higher margins, high attractiveness; the long-term potential is significant.

In simple terms: if the stock falls below €37, I would start building a position. The brand moat is intact, the name still commands a premium, and the restructuring pain appears to be largely front-loaded. The Q1 2026 results on April 29 will be the first real test of whether the recovery is materialising. Given how slowly things move in European industry, I expect Q2 results to give us a clearer directional read on where this company is actually heading.