Why Mercedes-Benz Isn't Turning the Corner Yet: My Look at 2025 Results and 2026 Guidance

Strong G-Class sales and a promising new CLA can't hide the bigger picture: Mercedes-Benz is losing ground in key markets, customer satisfaction lags, and 2026 guidance feels underwhelming. Here's what the numbers really mean for investors.

One of the leading premium automakers, which operates under the principle of “value over volume,” reported €132.2 billion in revenue for 2025 along with 1.8 million units sold in its Cars segment. Both figures show a decrease of 9.2% compared to the previous year. These numbers clearly indicate strong headwinds facing this automaker.

More than a year has passed since my last Mercedes-Benz review. To be honest, not much has changed. Revenue continues to decline, and Q4 - which is usually one of the strongest quarters - fell even faster than the year before. From a QoQ perspective, EPS dropped 44.3% and now stands at €1.43. On a YoY basis, MBG reports a decline of 47.6%.

When it comes to free cash flow on a yearly basis, the drop is even larger at 40.8%. In relative terms, this represents roughly twice the decline we saw a year ago, when the drop was 19%.

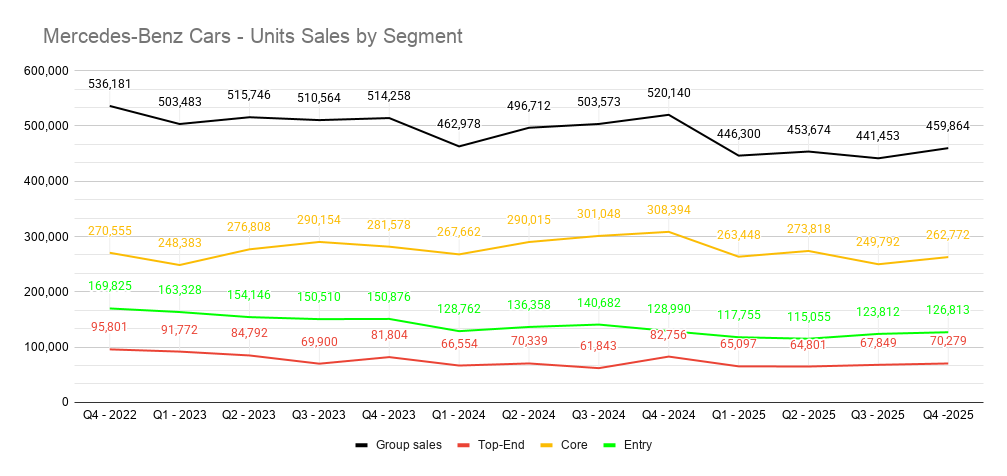

No Turnaround Yet: Mercedes-Benz Units Sold Decline Over 3 Years 1.8M in 2025 vs 2.04M in 2023

In last year's report, CEO Ola Källenius stated that we should start seeing real effects from the technological and product innovations made in 2024 during 2025 and 2026. We are still not seeing any meaningful improvement in the level of units sold. On the contrary, when we look at total units sold in the Cars segment, we can see a strong decline over the last three years. The company recorded 1.80 million units in 2025, 1.97 million in 2024, and 2.04 million units in 2023.

While the numbers on a quarterly basis do not look great (see graph above), the CEO points out that the new CLA (entry-level segment) is well accepted by the market and that the G-Class is achieving its strongest sales to date.

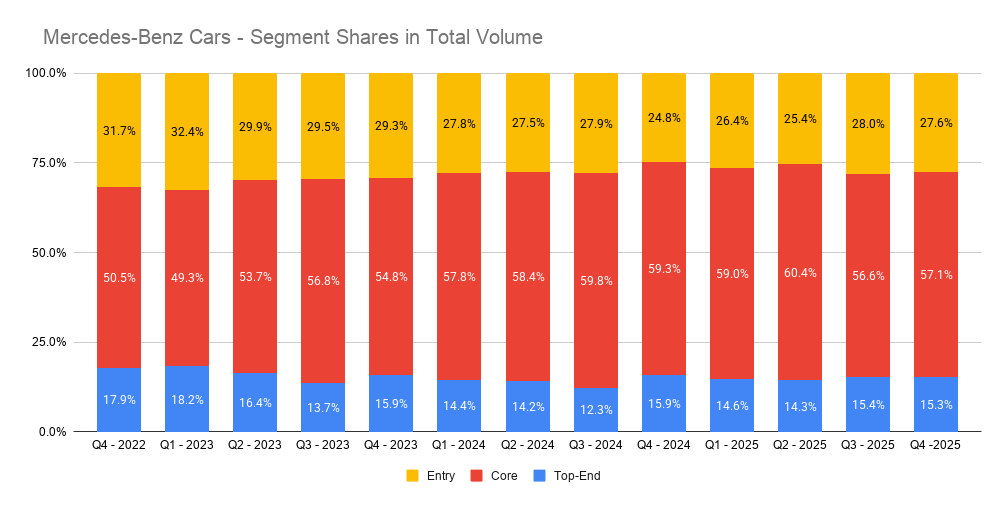

Here I would like to note that the company is focusing on increasing the share of Top-End vehicles in the last quarter. However, when we look at a slightly longer time scale, this increase is not that significant; especially when we consider the context of average selling price (ASP), which is 4% lower than last year (down from €71,000) and now stands just above €68,000.

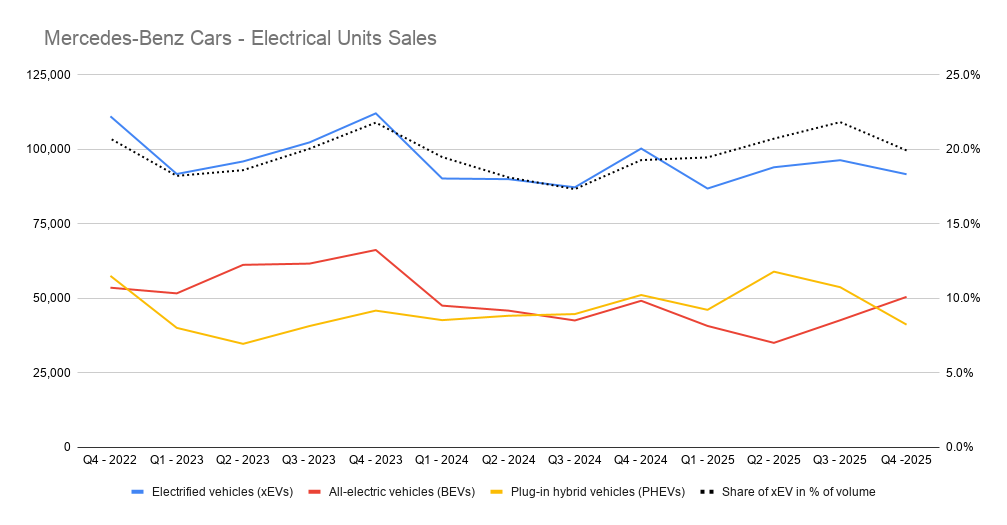

When we look at the electrification process, which the company has mentioned multiple times as successful, the numbers make it clear that it is hovering around 20%. This is below the percentages we saw in the same quarter in previous years.

Guidance Signals No Quick Recovery After 2025 Misses

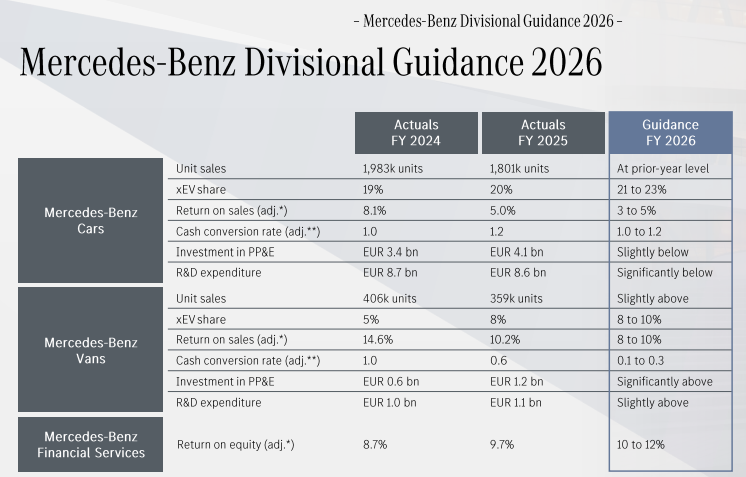

While the entire automotive industry continues to face strong headwinds, the company's guidance is what truly reveals its expectations for the future. And here lies the real problem. Investors had been assured that the technological innovations introduced in 2024 and the new product lineup launched in 2025 would finally begin to reverse the negative trends in the company's figures. Yet the guidance for 2026 is far from encouraging; particularly when we consider that this year's actual results came in at the lower end of last year's guidance range.

Is "Value Over Volume" Failing Mercedes-Benz? Volume Drops While China and USA Markets Shrink

Last year brought many unexpected challenges: tariffs, a saturated market in China, and intense competition from new players.

When we examine revenue by region, it becomes clear that the company is struggling to maintain sales outside Europe. In fact, Europe (including Germany) revenue declined only 1.5% year over year (with Germany down 3.5%), while the USA fell 11.2% and China dropped sharply by 28.6%.

For many years, Mercedes-Benz benefited from deep-pocketed buyers in Asia and the United States, where wealthy customers had few alternatives to European luxury brands. That landscape has now changed dramatically. Consumer preferences in transportation are evolving, and Mercedes is finding it increasingly difficult to attract customers outside Europe. Compounding the issue, customer perception surveys show that Mercedes vehicles receive the lowest satisfaction score (61) among major European high-end brands. This points to significant work ahead for the C-suite.

On a positive note, I am glad to see that Mercedes is actively trying to reach a broader customer base by expanding its entry-level offerings. Nevertheless, much remains to be done. Balancing the perception of a true luxury identity while making the brand more accessible to everyday buyers is a difficult challenge. The CEO's slogan "value over volume" sounded reasonable in theory, but the numbers tell a different story: volume is clearly decreasing. In my view, it may be time to rethink or refresh that slogan.

My Position on Mercedes-Benz

Not much has changed since my last Mercedes-Benz review a year ago. The share price is almost exactly where it was back then. We had plenty of opportunities to sell at higher levels or to buy on dips, but the stock has remained largely range-bound.

Last year delivered few positive surprises. I expected considerably more progress, yet the numbers remained weak overall, and the company's 2026 guidance shows no meaningful upward momentum. The strong emphasis on electric vehicles is positive in principle, but I would like to hear far more concrete discussion about charging infrastructure progress—something management highlighted one or two years ago but has not followed up on sufficiently.

I am currently averaging at €52 and plan to add to this position over time. I would be particularly inclined to increase exposure if the upcoming Q1 earnings report delivers results that beat expectations.

Analyst consensus for Mercedes-Benz in 2026 remains cautious but not outright bearish. The average price target sits around €60–€65 (implying 15–25% upside from current levels near €52), with most firms rating the stock as a Hold.